Insurance is not just a financial product; it is a safety net that protects your future during uncertain times. Many people purchase insurance policies without fully understanding what they actually need. Some choose plans because they are cheap, while others buy them based on recommendations from friends or advertisements. However, a policy that works perfectly for someone else may not be suitable for you.

Choosing the right insurance plan requires careful evaluation of your lifestyle, financial goals, family responsibilities, and future risks. A well-fitted insurance plan offers peace of mind, financial stability, and confidence during emergencies. Whether it is health insurance, life insurance, vehicle insurance, or travel coverage, selecting the right plan can save you from major financial stress later.

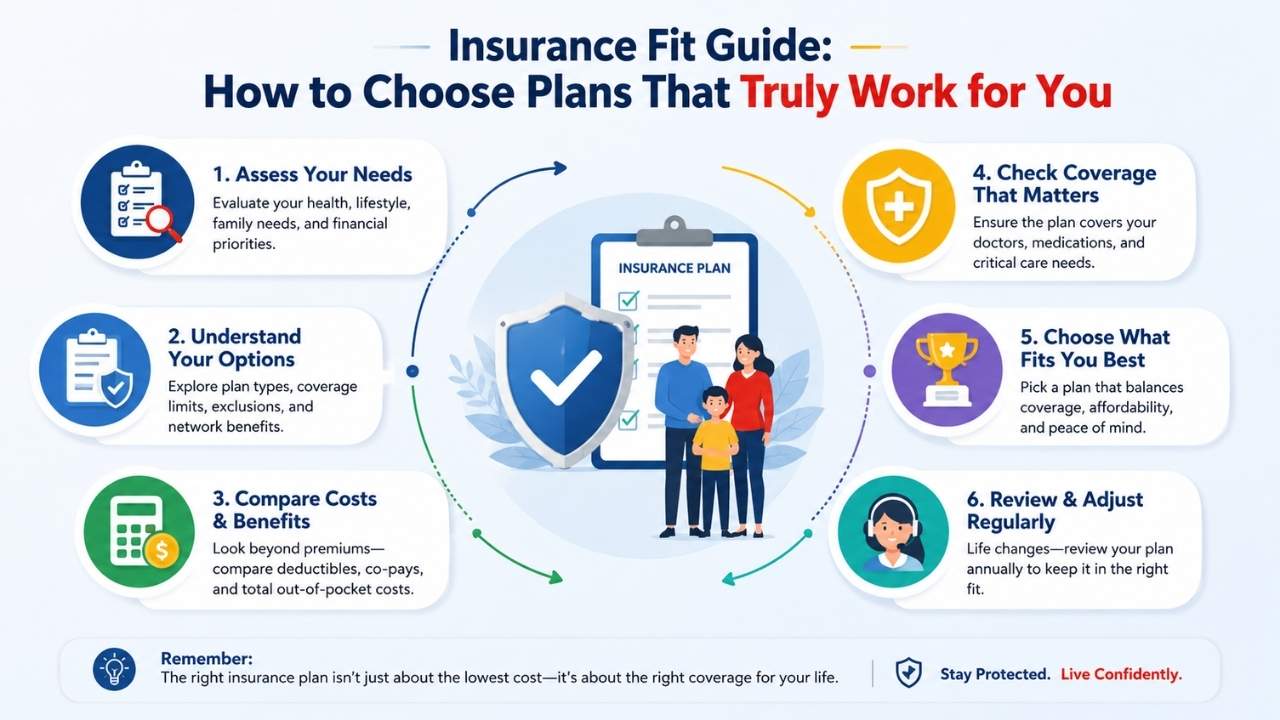

Start by Identifying Your Personal Needs

Before comparing plans, take time to understand your own requirements. Every individual has different financial situations and responsibilities. A young professional living alone may need different coverage compared to a married person with children.

Think about the following questions:

- Do you have dependents who rely on your income?

- How much savings do you currently have?

- What are your monthly expenses?

- Are you dealing with any existing health conditions?

- Do you own valuable assets that require protection?

Your answers will help you identify which type of insurance deserves priority. For example, if you are the main earning member of your family, life insurance and health insurance should become essential parts of your financial planning.

Know the Different Types of Insurance Plans

One of the biggest reasons people choose the wrong insurance policy is lack of understanding. It is important to know the purpose of each type of insurance before making a decision.

Health Insurance

Health insurance covers medical expenses such as hospitalization, surgeries, medicines, and emergency treatments. Rising healthcare costs make this one of the most important policies for individuals and families.

Life Insurance

Life insurance provides financial support to your family in case of your death. It ensures your dependents can continue managing household expenses, education costs, and loans without financial pressure.

Vehicle Insurance

Vehicle insurance protects you from repair costs, accidents, theft, and legal liabilities related to your car or bike.

Home Insurance

Home insurance covers damage caused by natural disasters, theft, fire, or accidents affecting your property.

Travel Insurance

Travel insurance offers protection against trip cancellations, medical emergencies abroad, lost baggage, and travel-related risks.

Understanding these categories helps you avoid buying unnecessary coverage while focusing on policies that genuinely support your needs.

Compare Coverage Instead of Only Comparing Price

A common mistake people make is choosing the cheapest policy available. While affordability is important, lower premiums often come with limited coverage, high deductibles, or hidden exclusions.

Instead of focusing only on the monthly or yearly cost, compare what each plan actually offers. Look closely at:

- Coverage limits

- Waiting periods

- Exclusions

- Claim settlement process

- Network hospitals or service providers

- Renewal benefits

- Add-on features

Sometimes paying a slightly higher premium provides significantly better protection and long-term value.

Understand Policy Terms Carefully

Insurance documents can seem confusing because of technical language and complex conditions. Many people skip reading the details and only discover limitations when filing a claim.

Always review the following sections carefully:

Exclusions

These are situations where the insurance company will not provide coverage. For example, some health insurance plans may not cover pre-existing illnesses during the initial years.

Deductibles

A deductible is the amount you must pay before the insurer starts covering expenses. Higher deductibles usually reduce premiums but increase your out-of-pocket expenses.

Claim Process

A smooth claim process is extremely important during emergencies. Check customer reviews and claim settlement ratios before selecting an insurer.

Waiting Periods

Certain policies require a waiting period before specific benefits become active. Understanding these timelines prevents future surprises.

Consider Your Future Financial Goals

Insurance planning should not only focus on current needs. Your future goals also matter. Marriage, children, buying a house, starting a business, or retirement can all change your financial responsibilities.

Choose plans that can adapt to your changing lifestyle. Flexible policies with upgrade options often provide better long-term value. Reviewing your insurance every few years helps ensure your coverage remains relevant as your life evolves.

For example, a single person may initially require individual health insurance, but later upgrading to a family floater plan may become more practical after marriage.

Check the Reputation of the Insurance Company

The quality of the insurer matters just as much as the policy itself. A company with poor customer support or delayed claim settlements can create major stress during emergencies.

Before purchasing any plan, research the insurer’s:

- Customer reviews

- Claim settlement ratio

- Financial stability

- Market reputation

- Customer service quality

Reliable insurers generally provide transparent communication, faster support, and smoother claim experiences.

Avoid Buying Unnecessary Add-Ons

Insurance companies often offer additional features or riders to increase policy benefits. While some add-ons are useful, others may simply increase your premium without offering real value.

Select riders that genuinely match your lifestyle and risk factors. For instance:

- Critical illness riders can be valuable for families with medical history concerns.

- Accidental coverage may benefit frequent travelers or drivers.

- Maternity coverage can help couples planning children.

Avoid purchasing every available add-on simply because it is recommended during the sales process.

Review Your Insurance Regularly

Insurance is not a one-time decision. Your financial situation, responsibilities, and health conditions can change over time. A plan that suited you five years ago may no longer provide enough coverage today.

Make it a habit to review your insurance annually. Update beneficiaries, increase coverage if needed, and remove unnecessary policies that no longer fit your lifestyle.

Regular reviews also help you take advantage of improved plans or better pricing available in the market.

Seek Professional Advice When Needed

If insurance terms feel overwhelming, speaking with a trusted financial advisor can help. An experienced advisor can explain policy details, compare options objectively, and guide you toward plans that align with your goals.

However, avoid making decisions under pressure from aggressive sales representatives. Take your time, ask questions, and fully understand the policy before signing any documents.

Final Thoughts

Choosing the right insurance plan is about creating financial security that truly matches your life. The best policy is not always the cheapest or the most popular one. It is the plan that protects your health, income, family, and future goals effectively.

By understanding your personal needs, comparing coverage carefully, reviewing policy terms, and planning for the future, you can make smarter insurance decisions with confidence. A thoughtful approach today can protect you from major financial difficulties tomorrow and give you peace of mind for years ahead.