Personal loans have become a popular financial solution for people who need quick access to funds for various purposes. Whether it is for medical emergencies, home renovation, higher education, debt consolidation, or a wedding, personal loans can provide immediate financial support without requiring collateral. However, taking a loan is a major financial responsibility that should never be approached casually. Before applying for a personal loan, it is important to evaluate several factors to ensure that the loan benefits your financial situation instead of creating additional stress.

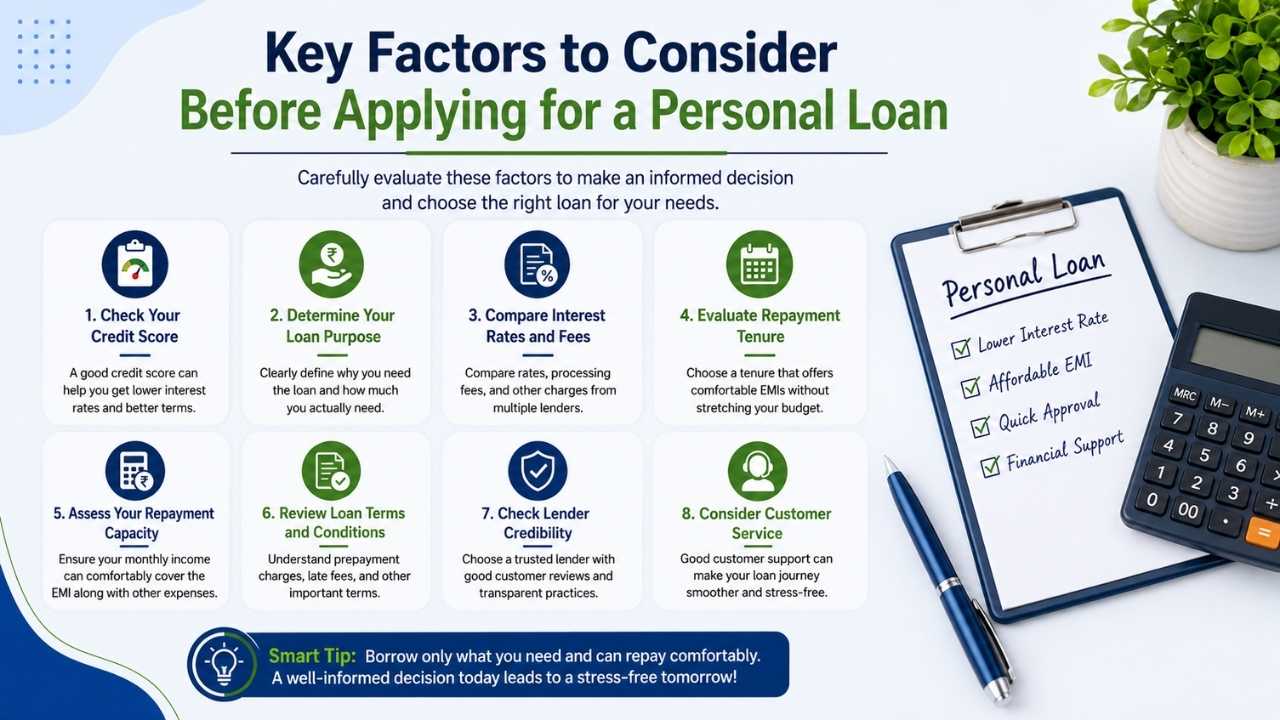

Understand Why You Need the Loan

The first and most important step before applying for a personal loan is understanding the exact reason for borrowing money. Many people take loans for unnecessary expenses and later struggle with repayments. A personal loan should ideally be used for important financial needs or situations that offer long-term value.

Ask yourself whether the expense can be delayed or managed through savings. If the answer is no, then a loan may be a practical option. Having a clear purpose also helps you determine how much money you actually need, preventing unnecessary borrowing.

Borrowing more than required may lead to larger monthly payments and higher interest costs over time. Responsible borrowing starts with understanding your financial priorities.

Check Your Credit Score Carefully

Your credit score plays a major role in personal loan approval. Banks and financial institutions use this score to measure your repayment behavior and financial reliability. A higher credit score usually increases the chances of approval and helps you secure lower interest rates.

Before applying, review your credit report and check for any errors or unpaid dues. If your credit score is low, consider improving it before submitting your application. Paying existing bills on time, reducing credit card balances, and avoiding multiple loan applications can positively impact your score.

Applying for a loan with poor credit may result in rejection or extremely high interest rates, which can increase your financial burden.

Compare Interest Rates From Different Lenders

One of the biggest mistakes borrowers make is accepting the first loan offer they receive. Interest rates can vary significantly between banks, credit unions, and online lenders. Even a small difference in interest rates can affect the total repayment amount.

Take time to compare loan offers from multiple financial institutions. Look beyond promotional advertisements and carefully read the actual annual percentage rate, commonly known as APR. This includes both interest and additional charges associated with the loan.

A lower interest rate can save a substantial amount of money over the loan period, making comparison an essential part of the borrowing process.

Evaluate Your Repayment Capacity

Before taking any loan, honestly assess your ability to repay it comfortably. Many borrowers focus only on loan approval and ignore future repayment responsibilities. This often leads to missed payments, penalties, and financial pressure.

Calculate your monthly income and existing expenses to understand how much you can realistically afford to pay every month. The loan EMI should fit comfortably within your budget without affecting essential expenses such as rent, groceries, education, or medical costs.

It is also wise to prepare for unexpected situations like job loss or emergency expenses. Taking a loan that stretches your finances too much can create long-term stress and damage your financial stability.

Understand the Loan Tenure

Loan tenure refers to the repayment period of the loan. Choosing the right tenure is important because it directly affects your monthly installments and total interest paid.

A shorter tenure usually means higher monthly payments but lower total interest costs. On the other hand, a longer tenure reduces monthly EMI amounts but increases the total repayment amount due to additional interest.

Select a tenure that balances affordability and overall cost. Avoid choosing a very long repayment period simply to reduce monthly payments, as it may become expensive over time.

Understanding how tenure affects your finances helps you make smarter borrowing decisions.

Be Aware of Hidden Charges and Fees

Many borrowers pay attention only to interest rates and ignore additional charges associated with personal loans. However, processing fees, late payment penalties, prepayment charges, and documentation fees can increase the total cost of borrowing.

Before signing any agreement, ask the lender for a complete breakdown of all applicable fees. Read the loan terms carefully to avoid unpleasant surprises later.

Some lenders may offer lower interest rates but compensate with higher hidden charges. Transparency is extremely important when choosing a financial institution.

Understanding all costs in advance helps you avoid financial confusion and better manage your repayment plan.

Read the Loan Terms and Conditions Properly

Loan agreements contain important details about repayment schedules, penalties, interest calculations, and borrower responsibilities. Unfortunately, many people sign documents without reading them carefully.

Take your time to understand every clause in the agreement. If anything seems unclear, ask questions before proceeding. It is always better to seek clarification rather than face issues later.

Pay special attention to conditions related to late payments, loan foreclosure, and changes in interest rates. Knowing your obligations in advance protects you from unexpected financial complications.

A well-informed borrower is less likely to face repayment problems.

Consider the Impact on Your Future Financial Goals

Taking a personal loan affects your future financial planning. Monthly EMI payments reduce disposable income, which may impact savings, investments, or future purchases.

Before applying, think about how the loan will fit into your long-term goals. For example, if you plan to buy a house, start a business, or invest in higher education in the near future, additional debt may limit your financial flexibility.

Responsible financial planning involves balancing current needs with future stability. Avoid taking unnecessary loans that may interfere with your larger financial objectives.

Choose a Trusted and Reputable Lender

Selecting the right lender is just as important as choosing the right loan. Work with banks or financial institutions that have a strong reputation for transparency, customer service, and fair lending practices.

Research customer reviews and lender credibility before making a decision. Reliable lenders provide clear information, professional support, and secure transactions.

Avoid lenders that make unrealistic promises, pressure you into borrowing more, or hide important details. Trustworthy financial institutions focus on responsible lending and customer satisfaction.

A good lender can make the borrowing experience smoother and more secure.

Final Thoughts

A personal loan can be a helpful financial tool when used wisely, but it also comes with significant responsibilities. Before applying, take time to evaluate your financial situation, repayment ability, credit score, and long-term goals.

Comparing lenders, understanding loan terms, and calculating the total borrowing cost can help you make informed decisions and avoid financial stress. Borrow only what you truly need and ensure that repayment fits comfortably within your budget.

Smart borrowing is not just about getting quick funds. It is about managing debt responsibly while protecting your financial future. By carefully considering these key factors, you can choose a personal loan that supports your needs without creating unnecessary financial pressure.